GNC the Latest Bankruptcy Casualty of Coronavirus

4 Arizona Locations to Close After Chapter 11 Bankruptcy Filing

As the coronavirus pandemic continues to wreak havoc on the global economy, more and more companies are filing for bankruptcy. This year has already seen retail giants like Neiman Marcus, JC Penney, J Crew, and True Religion file for Chapter 11 Bankruptcy. Huge fitness companies like Gold’s Gym and 24 Hour Fitness have also filed for bankruptcy protection amid the Coronavirus Pandemic. The latest big chain to file for Chapter 11 bankruptcy protection is GNC. The retail chain, which specializes in vitamins and dietary supplements, filed its bankruptcy petition June 23, 2020.

As the coronavirus pandemic continues to wreak havoc on the global economy, more and more companies are filing for bankruptcy. This year has already seen retail giants like Neiman Marcus, JC Penney, J Crew, and True Religion file for Chapter 11 Bankruptcy. Huge fitness companies like Gold’s Gym and 24 Hour Fitness have also filed for bankruptcy protection amid the Coronavirus Pandemic. The latest big chain to file for Chapter 11 bankruptcy protection is GNC. The retail chain, which specializes in vitamins and dietary supplements, filed its bankruptcy petition June 23, 2020.

What is Chapter 11 Bankruptcy? Why did GNC Choose Chapter 11?

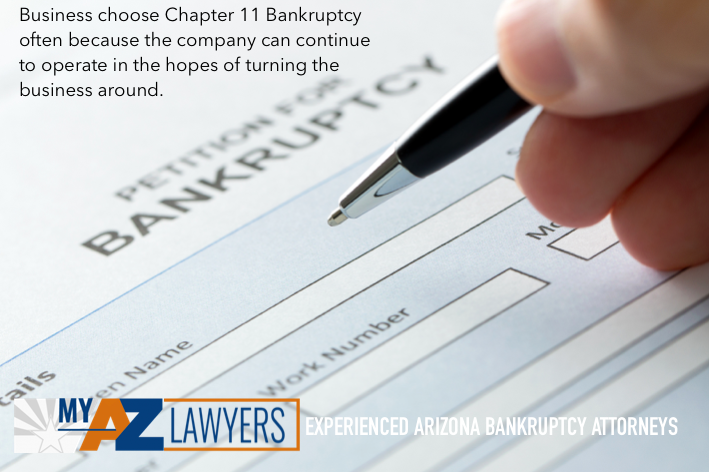

Chapter 11 Bankruptcy allows businesses and individuals with sizable assets and numerous liabilities to restructure their debt while being overseen and approved by the court and a panel of creditors. The panel, which is composed of the creditors the company owes the most money to, will have authority in major business decisions like entering contracts, taking out loans, and selling shares. However, in Chapter 11, the company can continue to operate in the hopes of turning the business around. Day-to-day operations remain in control of the company’s usual management. A company may still close down using Chapter 11 if settling the outstanding debts would be too complicated with other chapters.

The other chapter that businesses typically file is Chapter 7. Chapter 7 discharges unsecured debts and releases the owner/s of the company from personal liability, but the business must shut down and surrender all of its assets and inventory.

How the Pandemic Forced GNC to File Bankruptcy

GNC has posted statements to its website explaining its reasoning to file Chapter 11 bankruptcy. The company admitted that financial strains over the past few years had made the company unprepared to handle the pandemic and all of its negative economic effects. Like other brick-and-mortar chains, the competition posed by online retailers has caused GNC to struggle. GNC had already begun closing locations in shopping malls, widely considered to soon be a thing of the past, in 2018. The company had already amassed a staggering $1 billion in debts prior to its 2020 bankruptcy filing.

The company had plans to refinance and pay off its massive debts. Then the coronavirus pandemic hit. Starting in March, GNC was forced to close approximately 30% of its stores due to stay-at-home and quarantine orders. GNC reported first quarter losses of $200 million, where the chain had reported losses of $15 million for the same time period in 2019. While the company had its peak stock value of $60 per share in 2013, GNC’s stock value was less than a dollar- $0.81- shortly before the bankruptcy filing.

GNC’s Chapter 11 Bankruptcy Plan

GNC intends to remain open during and after the Chapter 11 bankruptcy, but to reemerge as a smaller company. The company currently has 5,800 locations and intends to almost 20%, or close to 1,200 of those United States locations. The company has already secured financing to fund its restructuring plan. IVC, GNC’s top vitamin supplier, has provided the company with $130 million in funding for the restructuring plan. The vast majority of GNC’s creditors approve of this plan, with a small minority left to sign on to the funding plan.

GNC intends to remain open during and after the Chapter 11 bankruptcy, but to reemerge as a smaller company. The company currently has 5,800 locations and intends to almost 20%, or close to 1,200 of those United States locations. The company has already secured financing to fund its restructuring plan. IVC, GNC’s top vitamin supplier, has provided the company with $130 million in funding for the restructuring plan. The vast majority of GNC’s creditors approve of this plan, with a small minority left to sign on to the funding plan.

If the funding plan from IVC falls through, the company also has the option to sell. Harbin is a Chinese pharmaceutical company that has 41% of GNC’s voting rights. Harbin, along with the rest of the Chapter 11 panel, have promised at least $760 million if the company is sold through court auction.

Arizona GNC Locations Impacted by Bankruptcy

Arizona is already struggling with a vast amount of new unemployment claims. More than 280,000 people in Arizona have lost their jobs due to the pandemic. GNC’s bankruptcy, and resulting store closures, will only add to Arizona’s climbing number of unemployment claims.

The following stores are closing as a part of GNC’s Chapter 11 Bankruptcy Plan:

- Madera Village, 9121 E. Tanque Verde Rd, Suite 115, Tucson, Arizona

- Grayhawk Plaza, 20701 N. Scottsdale Rd, Suite 105, Scottsdale, Arizona

- Flagstaff Mall, 4650 E 2 N Hwy 89, Flagstaff, Arizona

- Arrowhead Town Center, 7700 West Arrowhead Towne, Glendale, Arizona

There are more than 20 other GNC locations in Arizona that will remain open through the bankruptcy

Most individual bankruptcies are filed under either Chapter 7 or Chapter 13. Chapter 7 bankruptcy has strict income limits and the filer will have to surrender any assets with more equity than that state’s exemptions. Most unsecured non-priority debts will be discharged in Chapter 7. Credit cards, medical bills, repossession deficiencies, and more will be liquidated without any repayment. However, there is a caveat: debts that were fraudulently incurred can’t be discharged in Chapter 7.

Most individual bankruptcies are filed under either Chapter 7 or Chapter 13. Chapter 7 bankruptcy has strict income limits and the filer will have to surrender any assets with more equity than that state’s exemptions. Most unsecured non-priority debts will be discharged in Chapter 7. Credit cards, medical bills, repossession deficiencies, and more will be liquidated without any repayment. However, there is a caveat: debts that were fraudulently incurred can’t be discharged in Chapter 7.  Gambling debts are typically accrued in a few different ways. If you took out personal loans or credit cards to pay for your gambling, these debts may be discharged in bankruptcy. They will be wiped clean in Chapter 7 bankruptcy, and are lower priority debts that may only be partially paid before discharge through Chapter 13 bankruptcy.

Gambling debts are typically accrued in a few different ways. If you took out personal loans or credit cards to pay for your gambling, these debts may be discharged in bankruptcy. They will be wiped clean in Chapter 7 bankruptcy, and are lower priority debts that may only be partially paid before discharge through Chapter 13 bankruptcy.

Chapter seven bankruptcy is probably the most frequent kind of bankruptcy filed in the United States. Nevertheless, not everybody is permitted to obtain their debts discharged under Chapter seven of the U.S. Bankruptcy Code, so the following are a few simple demands for a situation. To understand whether you qualify for this particular case type, talk with a

Chapter seven bankruptcy is probably the most frequent kind of bankruptcy filed in the United States. Nevertheless, not everybody is permitted to obtain their debts discharged under Chapter seven of the U.S. Bankruptcy Code, so the following are a few simple demands for a situation. To understand whether you qualify for this particular case type, talk with a  Talk with a Chapter seven

Talk with a Chapter seven

Are you aware that if you owe $5000 on a credit card it could take over 20 years to pay it off making the minimum payment? Meanwhile the credit card company is getting rich off the interest you pay them. Although they would never admit it, credit card companies really don’t like customers who pay their bill in full each month, thus denying them all that interest. And heaven forbid you are late on your payments, that will incur large late fees and can legally allow the credit card company to raise your interest rate much higher. It’s all in the fine print. Once you get behind and those fees begin to rack up it’s a fast, downward spiral of ever increasing debt.

Are you aware that if you owe $5000 on a credit card it could take over 20 years to pay it off making the minimum payment? Meanwhile the credit card company is getting rich off the interest you pay them. Although they would never admit it, credit card companies really don’t like customers who pay their bill in full each month, thus denying them all that interest. And heaven forbid you are late on your payments, that will incur large late fees and can legally allow the credit card company to raise your interest rate much higher. It’s all in the fine print. Once you get behind and those fees begin to rack up it’s a fast, downward spiral of ever increasing debt. If you find yourself feeling anxious about your debt all the time, and lose sleep at night because you are worrying about your debt, it may be time to find your way out. The first step toward debt free living is the hardest. You have to sincerely decide that you are willing to do whatever it takes to get out of debt. It won’t be fast and it won’t be easy, but it will be worth it to once again enjoy worry free days and peaceful nights. Since the credit card companies want to keep you in debt, the only way out is to stop using them. Just cut them up. That may sound harsh, but if you are in credit card debt, you have been spending more money than you have been bringing in.

If you find yourself feeling anxious about your debt all the time, and lose sleep at night because you are worrying about your debt, it may be time to find your way out. The first step toward debt free living is the hardest. You have to sincerely decide that you are willing to do whatever it takes to get out of debt. It won’t be fast and it won’t be easy, but it will be worth it to once again enjoy worry free days and peaceful nights. Since the credit card companies want to keep you in debt, the only way out is to stop using them. Just cut them up. That may sound harsh, but if you are in credit card debt, you have been spending more money than you have been bringing in.  Perhaps you have been living beyond your means, or perhaps it’s due to circumstances beyond your control, such as medical bills. It boils down to the same problem, more money is going out than is coming in. So, the next step is to either to spend less or earn more. If you can find a way to do both, you can become debt free even more quickly.

Perhaps you have been living beyond your means, or perhaps it’s due to circumstances beyond your control, such as medical bills. It boils down to the same problem, more money is going out than is coming in. So, the next step is to either to spend less or earn more. If you can find a way to do both, you can become debt free even more quickly.

YOU SHOULD STOP FILING LAWSUITS

YOU SHOULD STOP FILING LAWSUITS

From 2005- 2010 all states showed an increase in

From 2005- 2010 all states showed an increase in

Also, you always want to keep in mind that the credit card holder wants to make money. That’s what they are in the business for. With interest, hidden fees, and other penalties, they make tons of money off other people, and they will try to do the same with you. If they don’t make money, the next thing they will try to do is not take a loss. They will do this at your expense, no matter how badly you are drowning in debt. Defaulting customers cost the creditors money, so they may compromise with you and get a portion of what’s owed to them instead of paying the collections agencies, implementing legal action, of having the debt discharged altogether when you file for bankruptcy. In addition to hurting you, it will also hurt the credit card holders. If you negotiate with the person you have called well enough, then you could reduce your debt a considerable amount and save yourself from horrible headaches in the future.

Also, you always want to keep in mind that the credit card holder wants to make money. That’s what they are in the business for. With interest, hidden fees, and other penalties, they make tons of money off other people, and they will try to do the same with you. If they don’t make money, the next thing they will try to do is not take a loss. They will do this at your expense, no matter how badly you are drowning in debt. Defaulting customers cost the creditors money, so they may compromise with you and get a portion of what’s owed to them instead of paying the collections agencies, implementing legal action, of having the debt discharged altogether when you file for bankruptcy. In addition to hurting you, it will also hurt the credit card holders. If you negotiate with the person you have called well enough, then you could reduce your debt a considerable amount and save yourself from horrible headaches in the future.

If you have already graduated with a mountain of student loan debt, there’s not much you can do about it now. Student debt cannot typically be discharged in a

If you have already graduated with a mountain of student loan debt, there’s not much you can do about it now. Student debt cannot typically be discharged in a